Financial Profiling & Optimization

Sometimes I wonder if I am spending too much money and should be saving more. It's tempting to try to micro-manage things by clipping coupons or skipping out on meals out with friends, but this strikes me as being similar to premature optimization of code, which as Knuth would say is the "root of all evil."

Just as it's not worth optimizing the 90% of the code where your program spends less than 1% of its time, it might not be worth packing your lunch every day to save a dollar a day ($250 per year) if your real problem is that you unnecessarily spend thousands of dollars on new laptops or other expensive equipment each year.

So what's the first step before I can figure out what to optimize? Profiling, naturally. About a year ago I grabbed a copy of MS Money, which is a personal finance tracking program. It can go online and download your bank account information and credit card statements. It tracks each transaction you make and uses heuristics to assign them to various expense categories. For example if Safeway is the merchant, it'll assign it to Groceries, if it's Comcast, then Utilities, and so on. Sometimes it doesn't know what a specific merchant should be assigned to so you have to configure it.

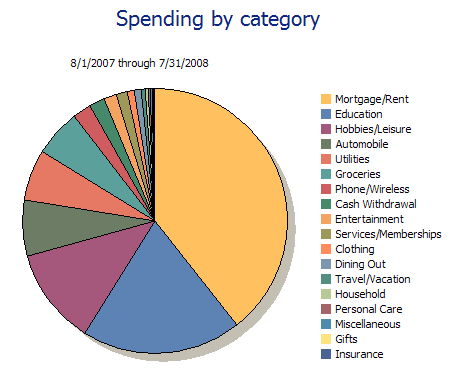

Once that's all set up, it can generate all kinds of plots showing your cash flow over time, estimated monthly budgets based on trended spending, and various other reports. Here's a pie chart of my spending over the last year:

Without this tool I would probably have had a hard time even estimating the percentage of my spending which goes into various categories, so it was quite interesting to see it charted like this.

The biggest item that jumps out of the chart is obviously "Mortgage/Rent", which in my case is just Rent. It accounts for nearly half of my spending, if you include Utilities (electricity, water, internet) along with it. I'm not sure whether this is a good or bad observation: on one hand I am spending a ridiculous amount of money on rent each month, but on the other hand it's nice to know that I'm not spending a similarly ridiculous amount of money on anything else.

"Education" is the next biggest category, which includes grad school tuition, fees, textbooks, etc.. I'm OK with spending a good chunk of money on this category since self-improvement and continual learning is a good thing. It's also nice that these expenses are completely reimbursed by Microsoft, so the chart of my "real" expenses should probably not even include this category (in which case Mortgage/Rent would fill more than half the pie).

Next biggest is "Hobbies/Leisure", which contains a large range of transactions, the largest of which are from "AMAZON.COM", "GAMESTOP/EBGAMES", "APPLE ONLINE" and "REI STORES." Overall I'm not too concerned about the current size of this pie slice since Hobbies/Leisure is basically the category for "what you do with your spare time," which, in the end, is the whole point of working and making money. I was a bit surprised at the total cost of my Amazon purchases over the last year - I could probably be a lot better about borrowing "read once" books from the library rather than buying them outright (Amazon Prime makes it too easy..).

"Automotive" is up next, which seems to be about equally split between car insurance and gas. I think I already have my car insurance pretty well optimized, so about the only way to reduce spending here is to drive less.

I'm lumping Utilities in with Mortgage/Rent, so "Groceries" is next. The final number in this category was another minor surprise and is probably a good area for optimization. Whole Foods organic milk and cereal apparently add up pretty quickly.

The rest of the spending categories don't sum up to much, so some of them are actually surprising for being so small. I'm disappointed that "Travel/Vacation" is almost not even visible on the chart. I hope that next year's chart will show Travel/Vacation making some big gains. "Gifts" is one category which is too small to show up, which would be totally pathetic of me if it weren't for the fact that most of my gift purchases were probably from Amazon and thus got stuffed into the Hobbies/Leisure slice.

One thing which is notably missing from this chart is money allocated to savings accounts & stock investments (I guess they aren't "Spending" since I still have the money). I had to generate a separate report for savings & stock investments and was pleased to find that the total number there was about equal to the total number in the Spending chart, which means that I have a savings rate of 50%, which is a lot better than the U.S. average, which is hovering around 0% even with the recent "stimulus" package.

Overall this was an interesting exercise to do. Now that I know the actual numbers I don't feel all that guilty about spending too much (except for in a couple of areas). In fact, I'm now feeling like I can probably afford to spend more, especially in "Travel/Vacation".

Me

Apps

Search

Archives

- July 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

August 6th, 2008 - 06:20

I think it’s GREAT that education is your second biggest category! A great investment…

It doesn’t look like there is a lot of room to cut back anywhere so that you can save more or use more for travel, unless you get a roomie…

Have to say this on the coupon cutting. While it might make me a nerd to do so, I save about $50 per month on coupons…I pay that much less to buy the same things for which many others pay full price. And I’m not a freak about it – I only cut coupons for brands/items I already use. That $50 is a little wiggle room to throw in the piggy bank, treat a friend to lunch or tuck away for vacation. Just a thought!

August 6th, 2008 - 10:16

Hmm $50 per month? That’s actually pretty good, and more than I thought. I should definitely look into whether I could save that much too.

It might also come down to how much time it takes to do this. For example if it takes 25 hours a month to save $50, then you’re only getting “paid” $2 per hour for that “work”. Of course I doubt it would take that much time..

August 6th, 2008 - 15:08

Your savings rate is fantastic – I am particularly impressed by that. I’d be interested to compare notes on your portfolio spread if you discuss that kind of thing.

I would guess I normally save about $50 a month on purchases, but I don’t clip coupons. I use a credit card for my monthly purchases (groceries, entertainment, etc) and pay it off in full every month. It’s a Target Visa, so I collect points towards 10% off each month, which I usually get most months. That alone saves a lot as I am a Target whore.

I also price check wherever possible. Go to Circuit City and instead of going to the checkout, go to the customer service desk and price check the item. Target, Best Buy and Walmart nearly always have any item for cheaper, and they will then match the price and give you a little more off. Once I asked to price check a DVD box set, and they asked where I wanted to match it to. I said “I don’t know… Target?” and a guy walked past and said “Walmart have it for $10 less”, so I asked them to price match it there! On two occasions they have given me the reduction twice (once after it was automatically applied). I refuse to pay full price for any major purchase and will delay the purchase until the price I want comes along.

August 6th, 2008 - 15:37

Yep in in that sense it is sort of nice to to own a house and have a high mortgage or any maintenance costs :). I guess I have my high savings rate right now in order to save up for a down payment someday.

When/if I do eventually buy a house, I will have a massive negative savings rate that year from the down payment.

I definitely need to get a new credit card like you have. Currently I don’t get much at all. I’m trying to decide whether to get one with cashback/retail points at Amazon/Target/etc, or get one that builds up frequent flyer miles instead..

I’ll check if Money can generate charts of portfolio spreads. That might be an interesting post.

August 7th, 2008 - 06:58

Eric –

I don’t invest that much time in coupon cutting, believe me – I can’t! I live in two cities (one during the week and one on the weekends), have a full time job and have a LOT going on during the week, plus all the fun stuff I like to do. Coupon cutting is not that difficult! It’s as simple as getting the Sunday paper and clipping the coupons you know you’ll need! I stick them in an envelope and quickly purge any old ones I know I won’t use before expiration. I make my grocery list and put a “c” next to the items for which I know I have a coupon. I make sure the envelope is either in my car or my work bag and boom! Savings! I probably spend a half hour total. It’s worth it to see dollars and dollars falling from my total at the end of my checkout.

August 15th, 2008 - 12:06

Thought you might want to know…I’m blogging!

August 16th, 2008 - 22:17

Cool! I’ll check it out 🙂